Upcoming Approvals, Momentum, and Shelf-Space Competition in Private Wealth

- mgoldberg57

- Oct 21, 2025

- 6 min read

Updated: Mar 10

Prepared by Mark Goldberg | October 23, 2025 | Research Note 4

Methodology & Interpretation Notes

This research note uses data from the 2025 Alts Leaders Survey, which tracks product approval activity across leading distribution platforms in the Wirehouse/Regional, Independent Broker-Dealer, and National RIA channels. Respondents collectively represent nearly 70% of all known private-wealth capital flows to private-market alternatives. The dataset includes both currently approved offerings and anticipated additions over the next 12 months across seven major asset classes: Private Credit, Infrastructure, Private Equity, Real Estate Equity, Real Estate Debt, Energy/Natural Resources, and Venture Capital. Product approvals serve as a key indicator of capital formation, revealing emerging strategies and platform momentum.

Executive Summary

While sales show where investor capital has already been invested, product approvals indicate where it is headed. Sales are a lagging indicator of market adoption, whereas approvals serve as a leading indicator of strategic direction. The pattern of approvals across asset classes offers an early glimpse of which strategies are gaining popularity with platform gatekeepers. As these approvals influence portfolio recommendations, they predict shifts in fundraising momentum and reveal how firms are positioning for the next phase of capital raising.

The Alts Leaders represent a cohort of firms whose collective decisions largely determine the trajectory of future capital formation. Each product approval represents an institutional commitment, not just to a single fund, but to the broader accessibility of that asset class within private wealth. Because these firms control the most visible and systematized platforms, their approvals effectively define the investable universe. This dynamic underscores why understanding the behavior and priorities of the Alts Leaders is essential: they are the mechanism through which market evolution occurs.

Findings & Interpretation

Across all Alts Leaders, Private Credit remains the most widely approved asset class, reflecting its alignment with demand for yield and stability. It anchors most platform lineups and remains the most likely category to receive incremental approvals. Private Equity follows as the next most common strategy, showing both strong current penetration and a high rate of expected additions, a sign that evergreen or semi-liquid structures are reshaping accessibility.

Infrastructure shows the steepest growth trajectory relative to its base, suggesting a broadening appeal linked to energy transition and digital infrastructure themes. Real Estate Equity and Debt maintain consistent representation, though new approvals are selective. Energy/Natural Resources and Venture Capital remain smaller but differentiated categories, attracting targeted approvals where thematic opportunities match specific advisor demand.

Distribution Segment Insights and Implications

The distinctions among distribution segments illustrate how each channel influences the growth of private markets. The data below shows the average number of offerings currently available on the respondents' platforms in their respective categories by asset class, including all registration types and structures. Wirehouse and Regional firms’ top category is Private Equity, with an average of 10.7 active offerings and plans to add another 6.9 in the coming year. Real Estate Equity is close behind at just over 10 approved offerings, though forecasted additions are modest at around two. Approvals for Real Estate Debt match those of Real Estate Equity, highlighting the increasing recognition of private credit within the real-asset sector. The Wirehouse/Regional model reflects institutional priorities: focusing on proven strategies, deliberate growth, and strict governance.

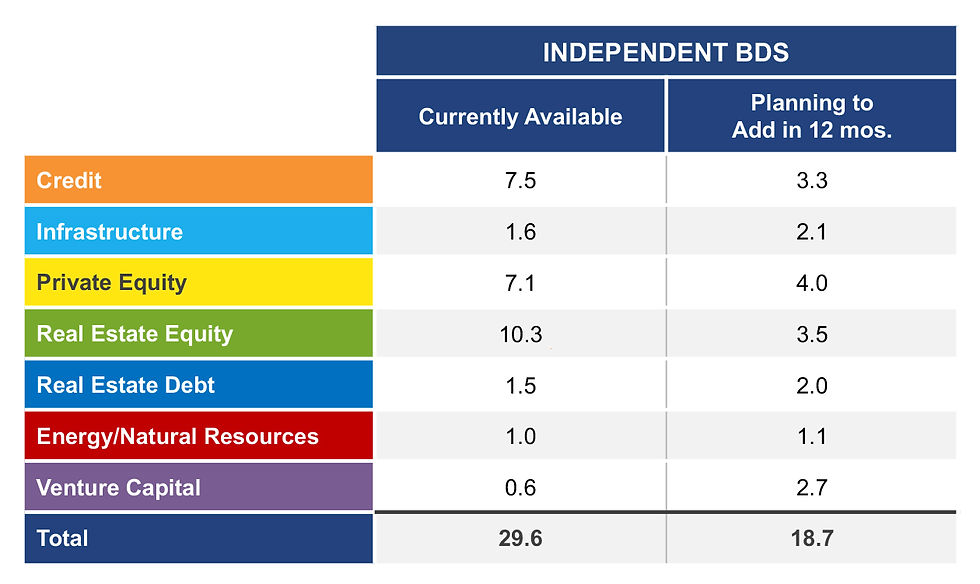

Independent Broker-Dealers (IBDs) exhibit the breadth and adaptability. They carry the highest average number of Real Estate Equity offerings (10.3) yet still plan to add 3.5 more, confirming strong advisor and investor appetite for tangible-asset income and reliance on DST 1031 exchanges as a tax deferment tool. IBDs also show higher openness to new Venture Capital offerings than Wirehouse/Regional peers, though not at RIA levels. Their approval mix spans Infrastructure, Real Estate Debt, and Energy/Natural Resources and underscores their flexibility and responsiveness to advisor demand for yield, tax efficiency, and diversification.

The National RIA segment is selective but increasingly influential. RIAs carry more Private Equity offerings than their peers and lead in Venture Capital approvals, with plans to expand both categories in the year ahead. This marks a pivotal evolution: RIAs are treating private markets not simply as diversification tools but as an alternative source of alpha relative to public equities. Their embrace of evergreen and semi-liquid structures reflects an intent to integrate private markets into core equity exposure, blending institutional access with fiduciary portfolio construction. In doing so, RIAs are redefining the boundary between public and private investing for the high-net-worth market.

Implications for Asset Managers Seeking Approvals

For asset managers, understanding the distribution of product approvals across channels helps guide engagement strategies and resource allocation. Each channel’s approval patterns reflect a specific investment philosophy and openness to innovation. Wirehouse and regional firms focus on institutional alignment and scale, IBDs prioritize flexibility and engagement, and RIAs seek innovation, liquidity, and strategies that generate equity alpha. Approvals reveal the current market trend. Those who adapt their product design and communication accordingly are more likely to gain platform access.

Existing approved sponsors benefit from established relationships and shelf presence, translating into faster reviews (sponsor Due Diligence and operational fit completed) and incremental approvals. For new entrants, the implication is clear: success requires differentiation, persistence, and readiness to meet the institutional standards and governance expectations of each channel. Given the number of approvals and the chance that the same funds get approved at multiple firms, the competition for “shelf space” is already fierce.

Implications for Distribution Partners

The surge in interest in private markets and the growing number of fund offerings place enormous resource demands on distribution partners to review, diligence sponsors, and support offerings that are ultimately approved. Firms have adopted a range of strategies to manage these pressures. The methods include pivoting to using more evergreen funds than calendar products, being more selective about which funds advance to review, partnerships with third-party due diligence, and expanding internal teams. There are also some fascinating but fledgling initiatives to use AI tools to enhance fund selection, streamline reviews, and monitor existing fund offerings.

Opportunities by Asset Class and Channel

The approval patterns show that while Private Credit and Private Equity remain the most widely distributed strategies, the size and direction of growth vary by segment. Wirehouses continue to formalize Private Equity (10.7 active, 6.9 planned) and Credit (8.1 active, 3.7 planned). IBDs display the broadest opportunity set with Real Estate Equity (10.3, 3.5) and Venture Capital (0.6, 2.7), highlighting diversification momentum. RIAs lead the next frontier, growing in Private Equity (12, 7) and Venture Capital (3.8, 3.8), as they reposition private markets as equity replacements. The heat map below shows planned additions across asset classes and distribution channels. Darker green cells highlight where the greatest number of new approvals is expected in the next 12 months and point to the best opportunities for asset managers. Please note that the heat map reveals where shelf space opportunities exist in the short term, while shifts in capital allocations are more likely to happen over the medium and long term.

Approvals Pipeline by Asset Class and Channel

Absolute Planned Additions – Alts Leaders Survey 2025

Source: Alts Leaders Survey 2025 | Alternative Investments Market Intelligence

Approval Momentum by Asset Class and Channel

While the previous chart shows where most product approvals are expected in the next 12 months, the heat map below captures the rate of change, showing how quickly each asset class is expanding relative to its existing presence on platform line-ups.

Darker green tones indicate higher forward-approval momentum, where the ratio of planned additions to current offerings is steepest. These are the segments where platforms are leaning most aggressively into innovation and new access points.

The data show that Venture Capital within Independent Broker-Dealers and Energy / Natural Resources across all channels experience the highest relative growth momentum. The small amount of funds and low level of capital formation in the last category should temper the view that Energy/Natural Resources present a significant opportunity. Infrastructure and Real Estate Debt also show meaningful expansion, indicating that product development in these categories is accelerating.

Taken together, the two heat maps reveal the scale and velocity of approval activity - pointing to where product development, due diligence, and capital formation are most likely to converge over the coming year.

Approval Momentum by Asset Class and Channel

(Planned ÷ Current Approvals)

Looking Ahead

While this note focuses on product approvals by asset class and channel, the next research note will concentrate on sector-specific strategies in favor. Early data indicate growing interest in sports and media investments, as well as a renewed focus on student housing, data centers, and industrial real estate. This likely reflects the belief that each is linked to strong demand drivers such as experiential ownership (sports and media), consistent out-performance (student housing), digital infrastructure (data centers), and supply-chain resilience (logistics). Upcoming research will explore these trends in detail, illustrating how innovation, distribution, and capital formation come together to shape the next stage of private-market growth and which investment structures are favored by Alts Leaders.